For Vanillas & vol derivatives (VIX, var, vol swaps)

And many others...

Built for options desks

auto fa = makeFactoryAnalytics();

auto fp = std::string("AEX_20160622-160000.000-CET_ocpf-eq.json.gz"); // serialized price fitter

auto ocpf = fa->makeOptionChainPricerFitterEquity(fp); // create fitter from serialized instance

auto oc = ocpf->optionChain(); // the option chain with contract information

auto ps = ocpf->priceSnapshot(); // price snapshot with price information

auto vcts = VecVCT{ VCT::C6, VCT::C10M }; // curve type to use for fitting vols

auto rf = ocpf->fit(ps, vcts); // fit price snapshot

auto vs = rf->volSurface(); // use the volsurface for pricing

auto ocp = fa->makeOptionChainPricerEquity(oc, vs) // create pricer

auto rp = ocp->price(); // compute prices and greeks for all options in the option chain

Trade any index, ETF/stock, or futures options in any asset class (equity or FICC) off auto-fitted and/or easily adjusted surfaces.

Market maker quality valuations and vol surfaces in milliseconds.

Drop-in replacement for critical pricing and fitting infrastructure (C++, Python, Java, C#).

Supported directly by the quants who build it.

e.g. via "SSR", is integrated throughout, for accurate "smart" delta and gamma, realistic spot scenarios (incl. overnight), and temporal smoothing without bias.

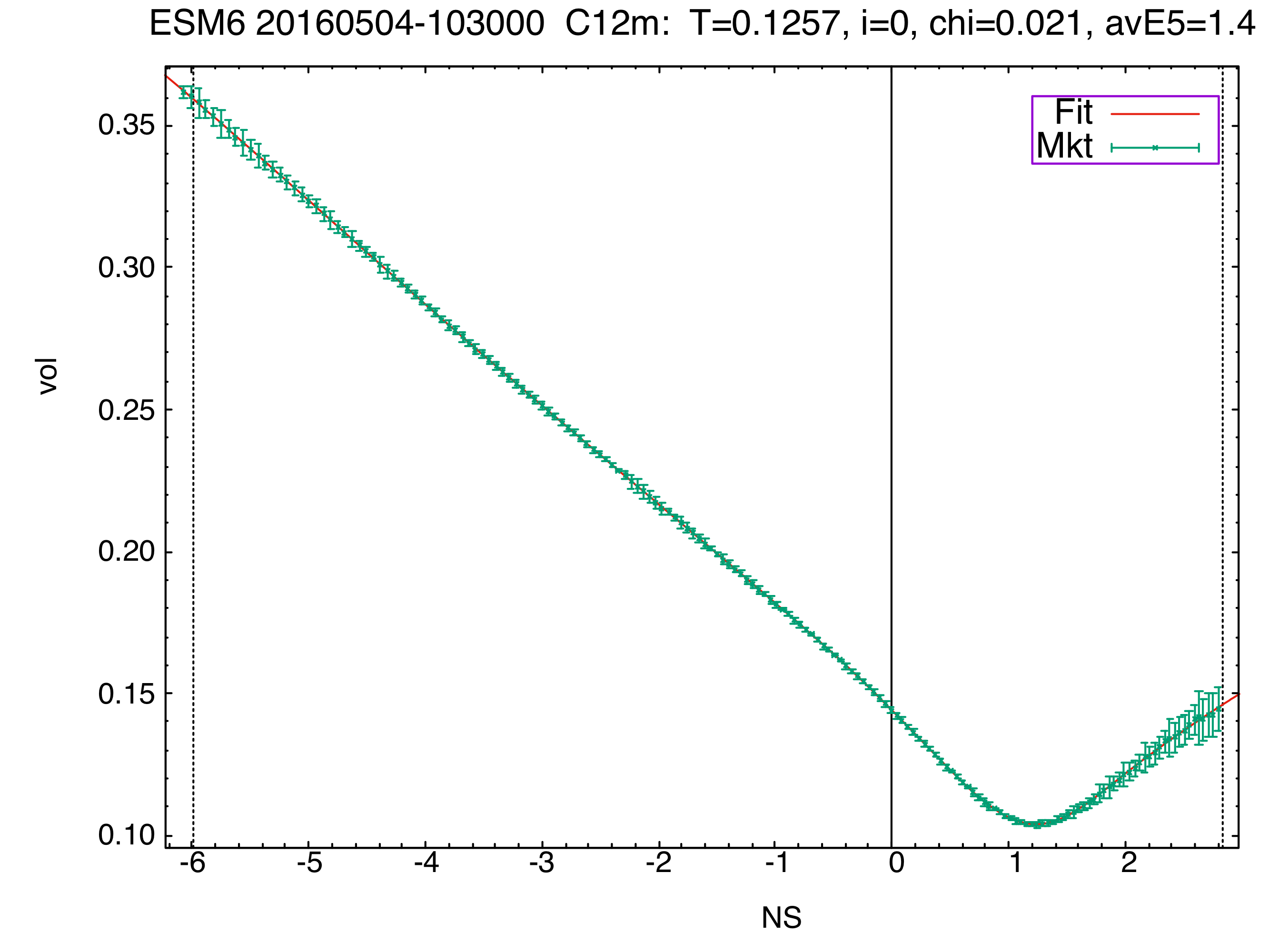

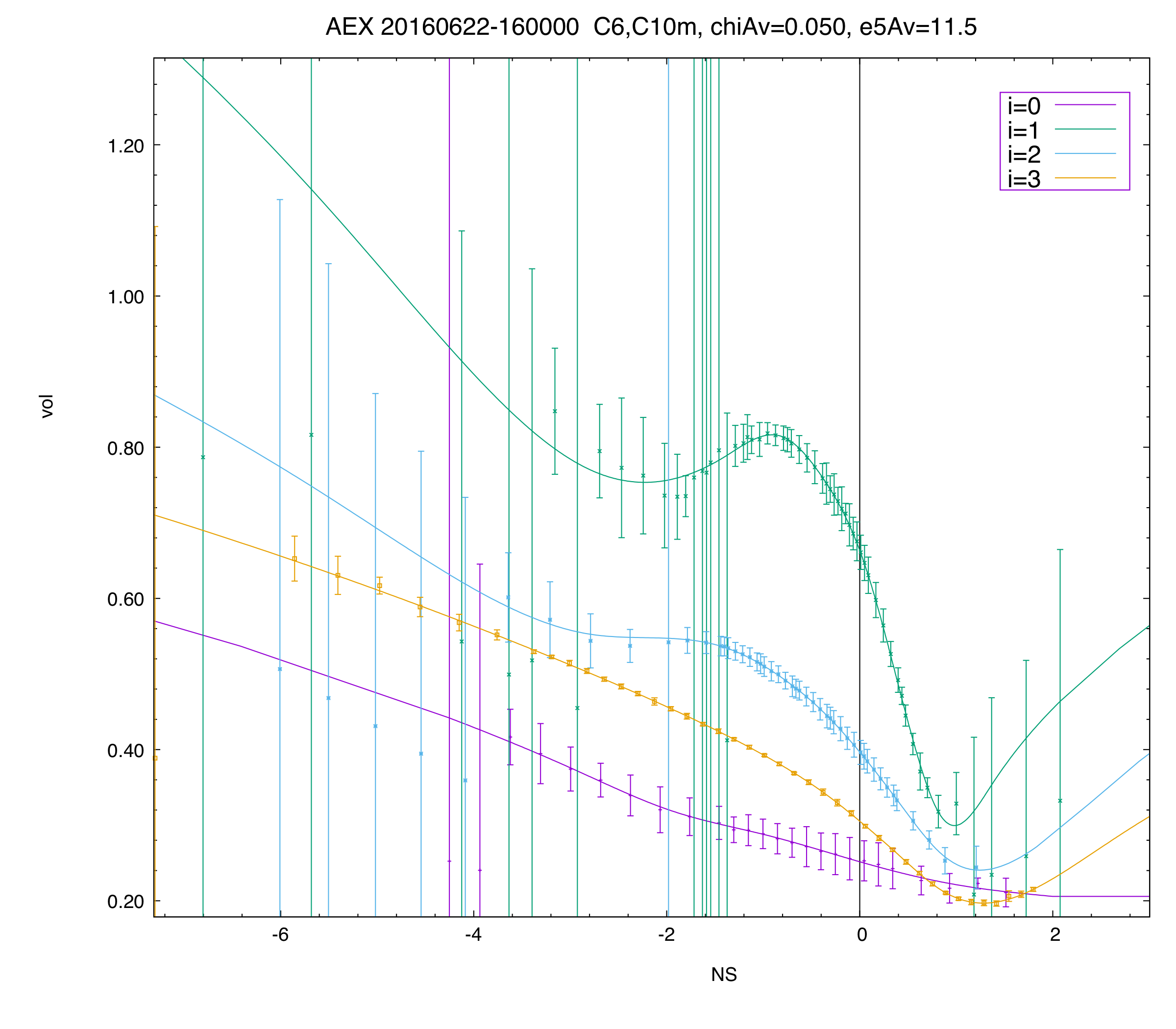

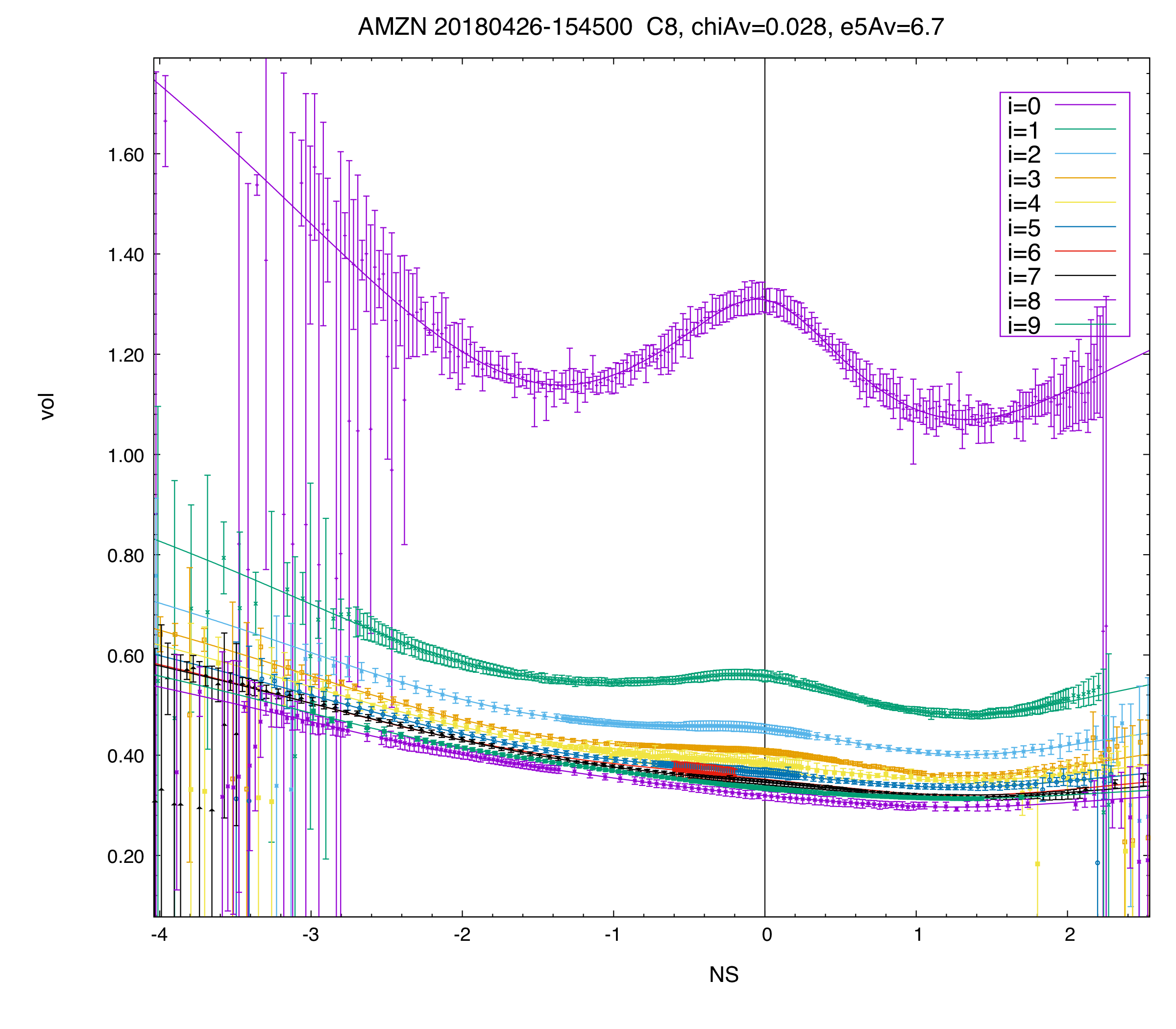

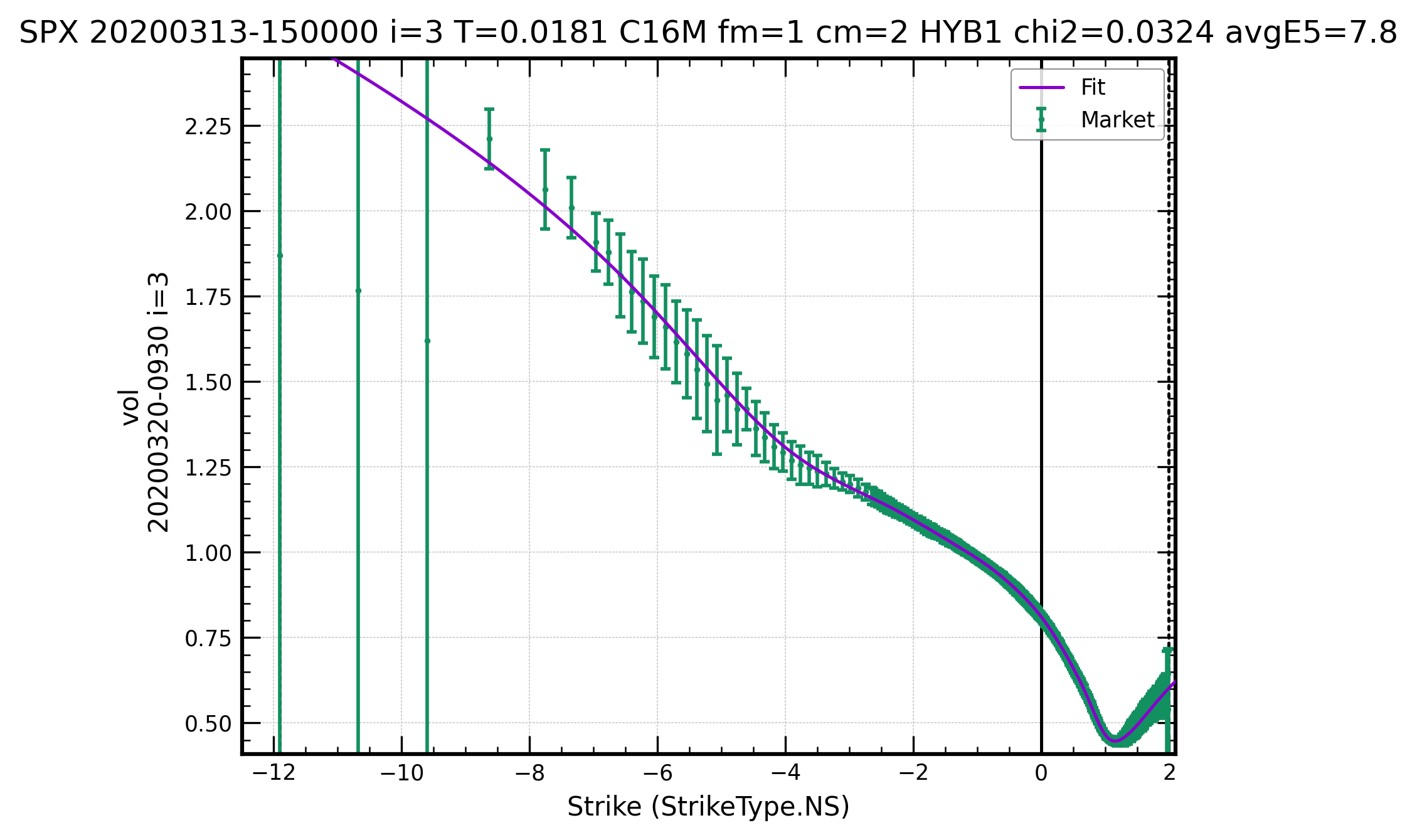

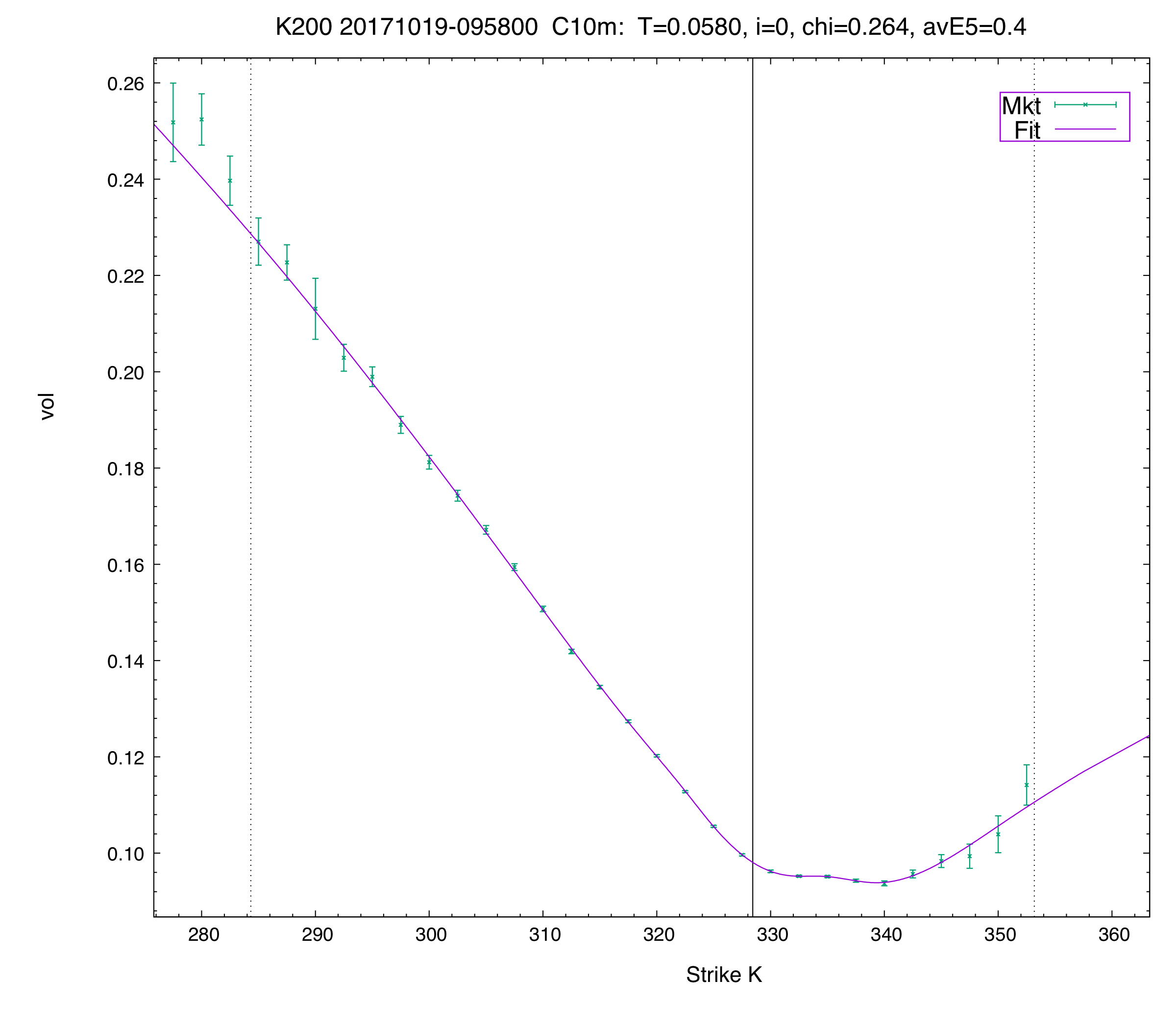

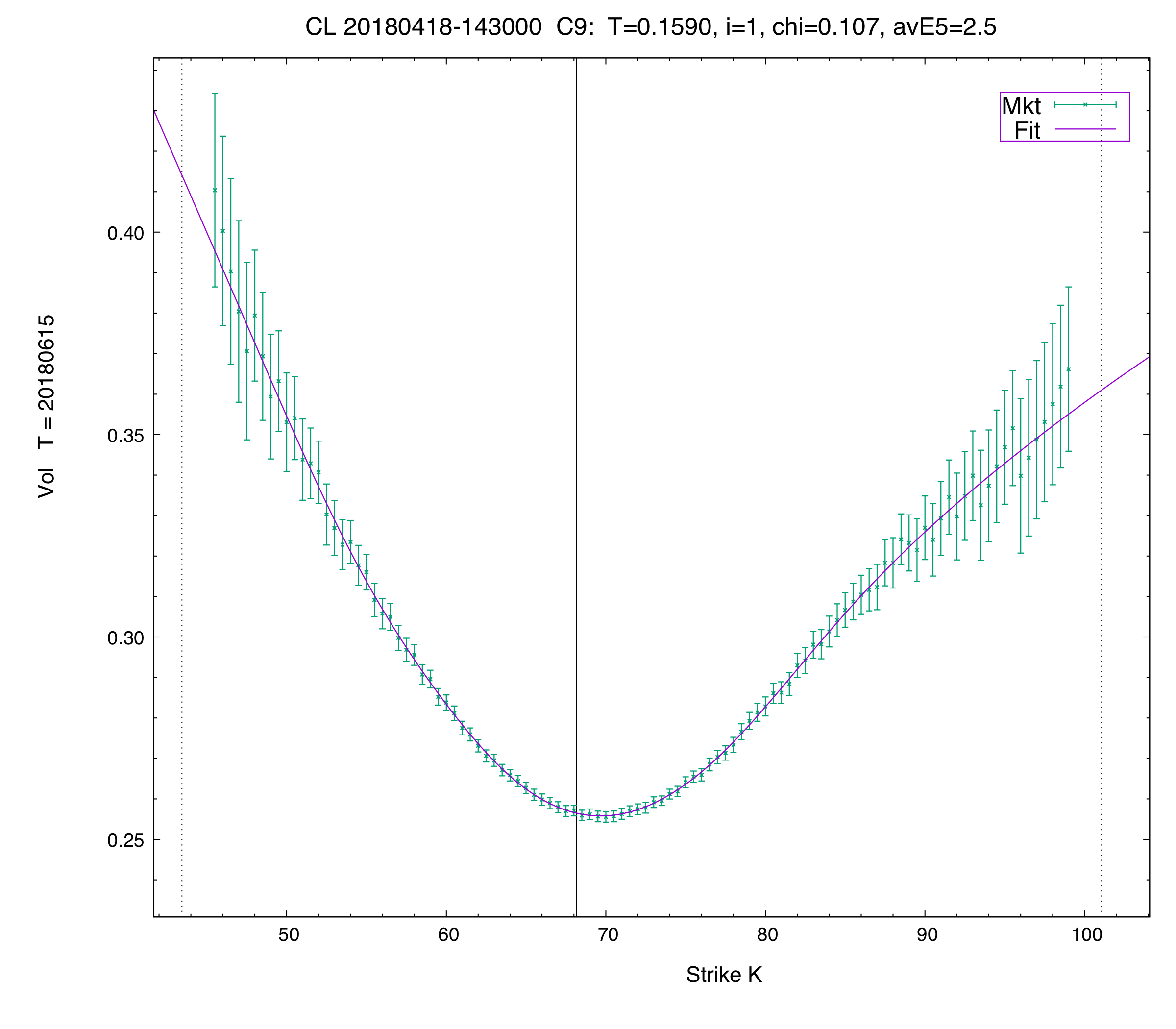

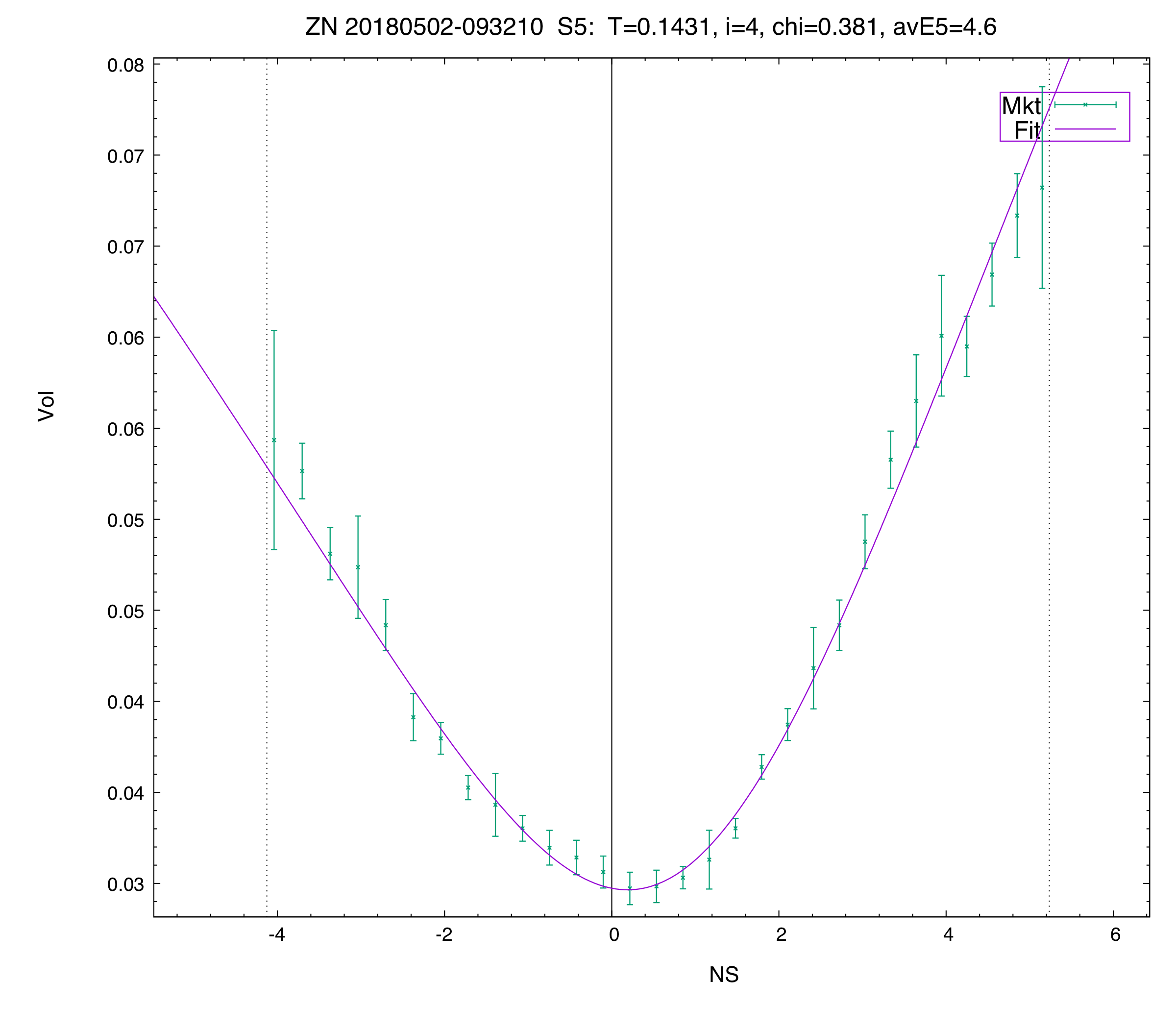

Fit even the most liquid names like SPX, SPY, ES, NVDA, TSLA, etc, including around events or periods of market turmoil.

Way beyond simple curves like SABR, SSVI, SVI (which are also available).

Accurate and flexible, including "blending schemes", large borrows (HTB), funding curves, etc.

Fast, accurate and robust for any dividend model.

Delta, gamma, vega, volga, vanna, rho, rhoBorrow, rhoDiv, thetas (with regard to rate or vol time), fugit.

Allow intuitive stabilization of vol surfaces even if data become very sparse over extended periods.

Universal and intuitive across all curve types. Extend vol surfaces beyond listed expiries, or proxy to other names, etc.

Rate term-structure pricing, vol-time, events, and settlement effects.

Our clients trust Vola Dynamics to maintain their core valuation and risk analytics (pricing, greeks, volatility surface fitting, scenario analysis) for equity, futures and index options.