Battle-tested

For Vanillas & vol derivatives (VIX, var, vol swaps)

Trusted by the world's best

market makers

vol arb traders

prop shops

hedge funds

asset managers

banks

valuation agents

prime brokers

exchanges

clearing houses

regulators

trading platforms

And many others...

Built for options desks

Why Vola?

- Do you need a fast, robust, and accurate options pricer for valuations and greeks?

- Do you need a robust, real-time borrow and volatility fitter for electronic trading?

- Do you need stable, arbitrage-free vol surfaces to feed into your LV or SLV model?

auto fa = makeFactoryAnalytics();

auto fp = std::string("AEX_20160622-160000.000-CET_ocpf-eq.json.gz"); // serialized price fitter

auto ocpf = fa->makeOptionChainPricerFitterEquity(fp); // create fitter from serialized instance

auto oc = ocpf->optionChain(); // the option chain with contract information

auto ps = ocpf->priceSnapshot(); // price snapshot with price information

auto vcts = VecVCT{ VCT::C6, VCT::C10M }; // curve type to use for fitting vols

auto rf = ocpf->fit(ps, vcts); // fit price snapshot

auto vs = rf->volSurface(); // use the volsurface for pricing

auto ocp = fa->makeOptionChainPricerEquity(oc, vs) // create pricer

auto rp = ocp->price(); // compute prices and greeks for all options in the option chain

Why Teams Choose Vola

Flexible & Intuitive

Trade any index, ETF/stock, or futures options in any asset class (equity or FICC) off auto-fitted and/or easily adjusted surfaces.

Robust & Fast

Market maker quality valuations and vol surfaces in milliseconds.

Easy Integration

Drop-in replacement for critical pricing and fitting infrastructure (C++, Python, Java, C#).

Supported directly by the quants who build it.

A Complete Volatility and Pricing Infrastructure

The surface feeds pricing, pricing feeds Greeks, Greeks feed hedging and PnL — and at every step, the requirements are in tension. Accurate and fast. Smooth and flexible. Robust and arbitrage-free.

-

Proper spot-vol dynamics

e.g. via "SSR", is integrated throughout, for accurate "smart" delta and gamma, realistic spot scenarios (incl. overnight), and temporal smoothing without bias.

-

Bias-free fits of arbitrary market vol shapes including W-shapes

Fit even the most liquid names like SPX, SPY, ES, NVDA, TSLA, etc, including around events or periods of market turmoil.

-

Intuitive and flexible parametric curves

Way beyond simple curves like SABR, SSVI, SVI (which are also available).

-

Cash dividend & forward modeling

Accurate and flexible, including "blending schemes", large borrows (HTB), funding curves, etc.

-

Implied borrow, forward and vol calculations

Fast, accurate and robust for any dividend model.

-

All greeks

Delta, gamma, vega, volga, vanna, rho, rhoBorrow, rhoDiv, thetas (with regard to rate or vol time), fugit.

-

Flexible temporal filtering and priors

Allow intuitive stabilization of vol surfaces even if data become very sparse over extended periods.

-

Vol surface shape transformations

Universal and intuitive across all curve types. Extend vol surfaces beyond listed expiries, or proxy to other names, etc.

-

Subtleties for modern markets

Rate term-structure pricing, vol-time, events, and settlement effects.

Products

- Super-fast and robust pricing of European and American vanillas, with accurate handling of cash dividends.

- Prices the whole US options universe on one box in a fraction of a second (without a table method!).

- Choice of several dividend pricing models actually used by the most successful options trading firms.

- Covers options on stocks, ETFs, futures, and indices.

- Handles large borrow costs and any number of cash dividends.

- Has all greeks: delta, gamma, vega, volga, vanna, rho, rhoBorrow, theta, fugit.

- Smart delta and gamma account for how vol moves when spot moves (the Skew Stickiness Ratio). The correction to Black-Scholes delta can be several percentage points for index options.

- Two thetas, reported separately: vol-time theta (how much optionality decays) and calendar-time theta (how much interest accrues). A straddle has mostly vol-time theta; a box has only calendar-time theta. They are different risks.

- Configurable time conventions: calendar days, trading days, event-adjusted — match your existing desk framework.

- Discrete one-day theta: the actual P&L from holding overnight, accounting for weekends, holidays, and events.

- Fast and accurate implied vol calculation for any dividend model.

- Super-fast and robust. Fit the whole US options universe on one box!

- Based on modern Bayesian ideas, superior numerics, and 30 years of trading and research. Robustness is achieved by transferring information across strikes, expiries and time (filtering).

- Uses unique set of flexible and intuitive curves (see Curves for details), allowing smooth and bias-free fits of all observed skews in the market.

- Adjust volatility surfaces between fits using proper spot-vol dynamics.

- The fitter can produce stable, arbitrage-free volatility surfaces even in the far wings, beyond the range of listed options, as required for the calibration of the various “SLVJ” models used for exotics and structured products.

- Output error bars derived from input bid-ask spreads quantify uncertainty in each fitted vol. For market makers, they serve as a natural “minimum edge” — if the market price is within the error band, there is no statistical confidence that edge exists.

- Graduated defense: when data quality degrades (stale quotes, exchange glitches, erratic markets), error bars widen automatically, making the system more conservative without hard kill switches.

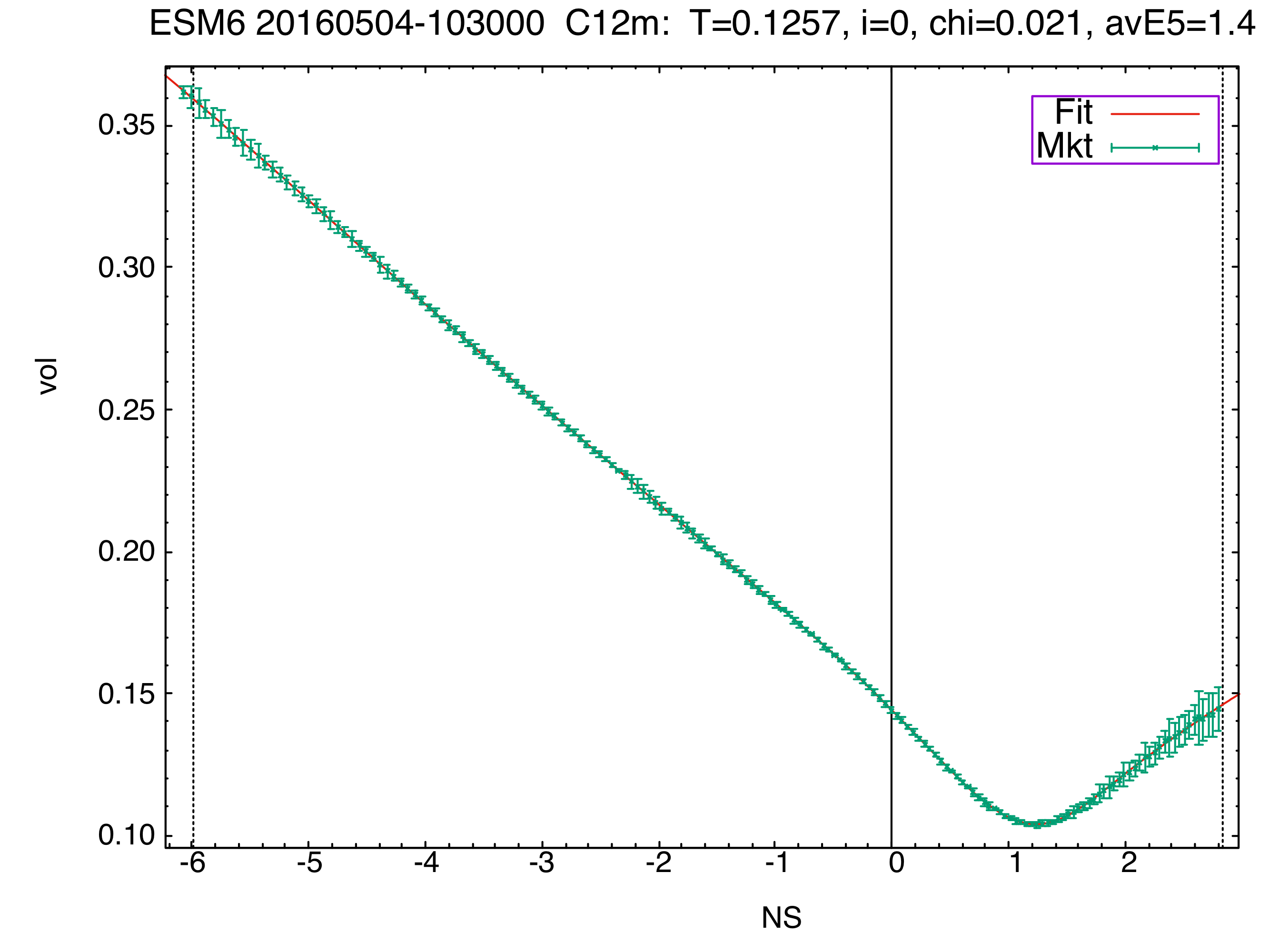

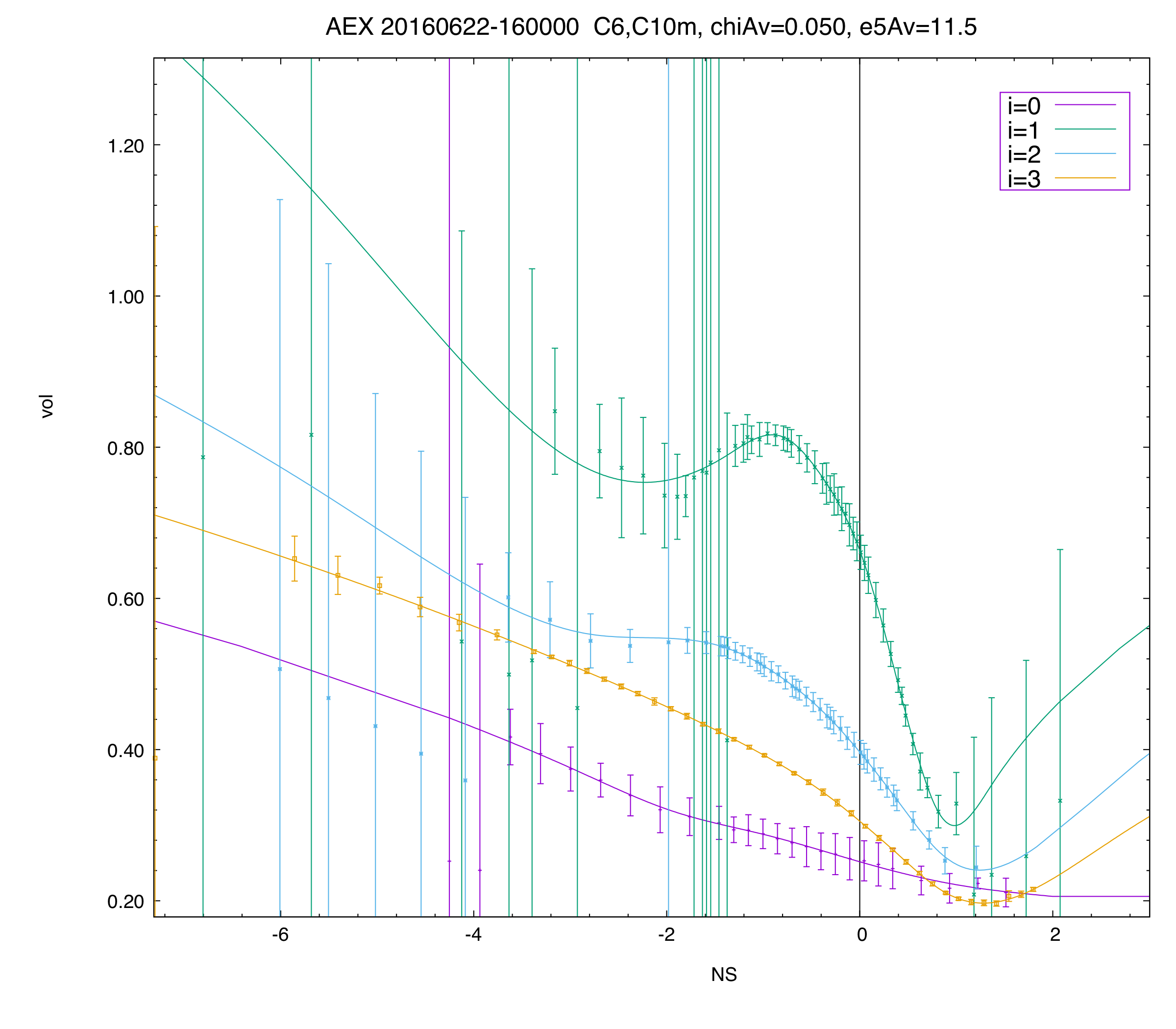

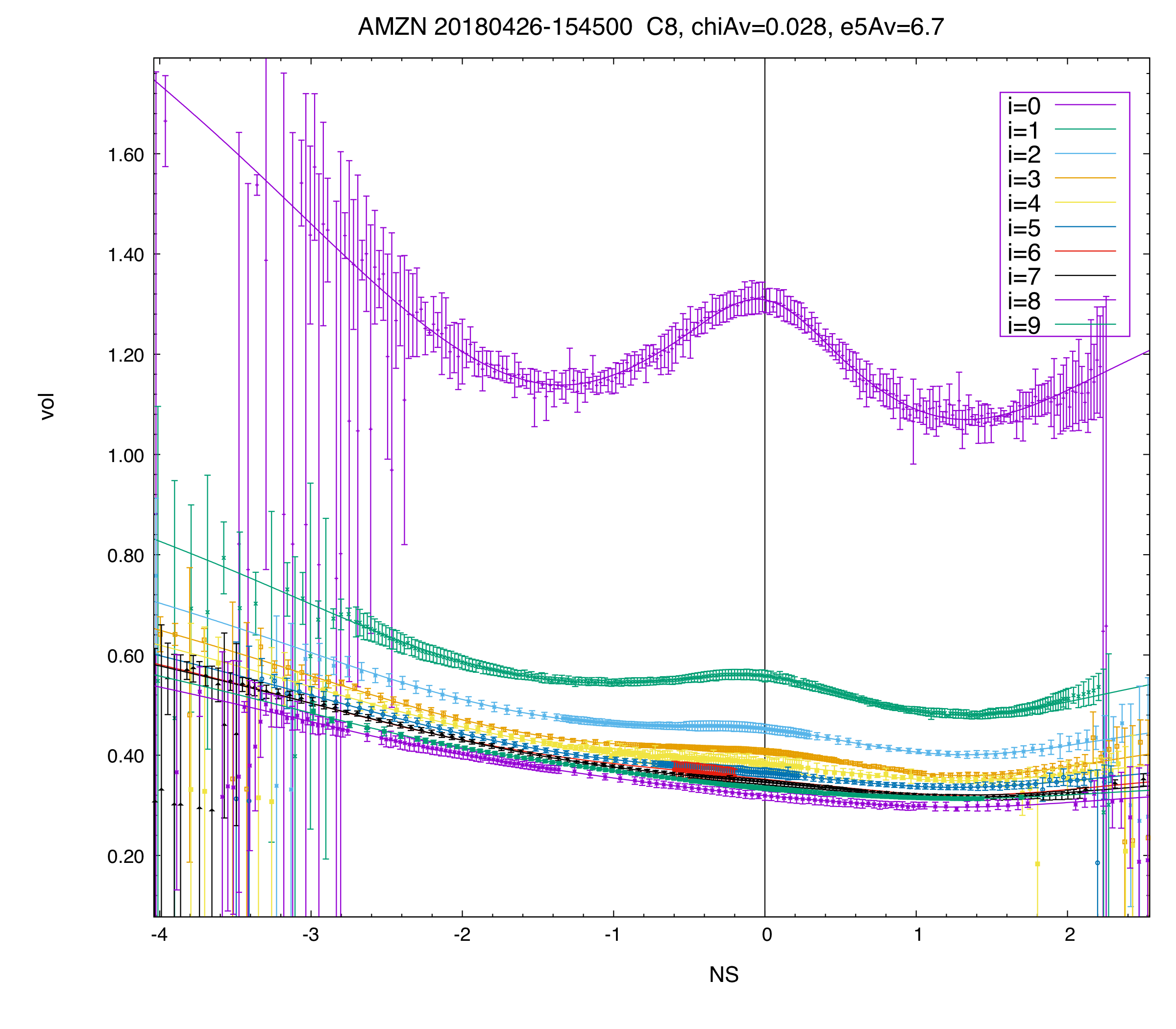

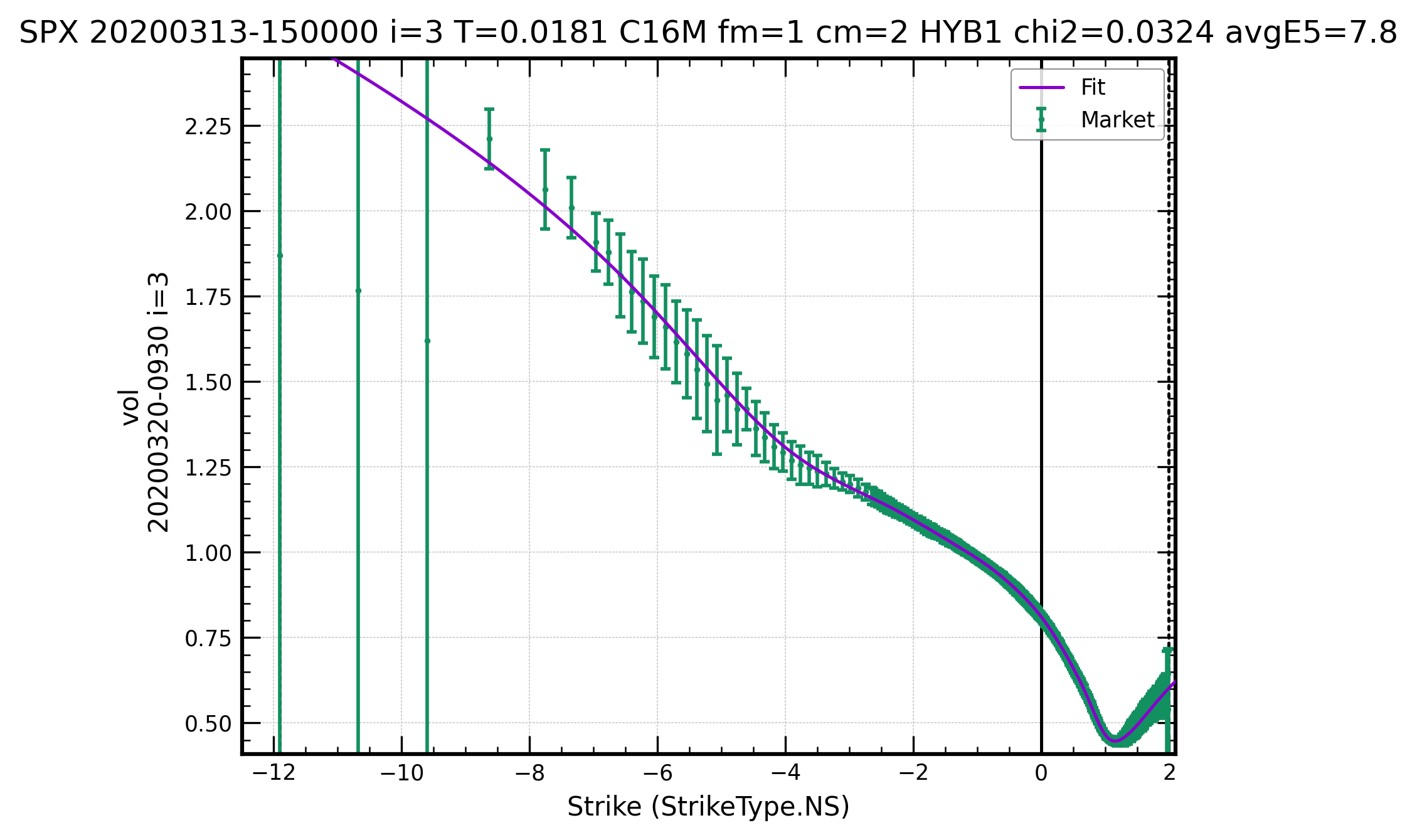

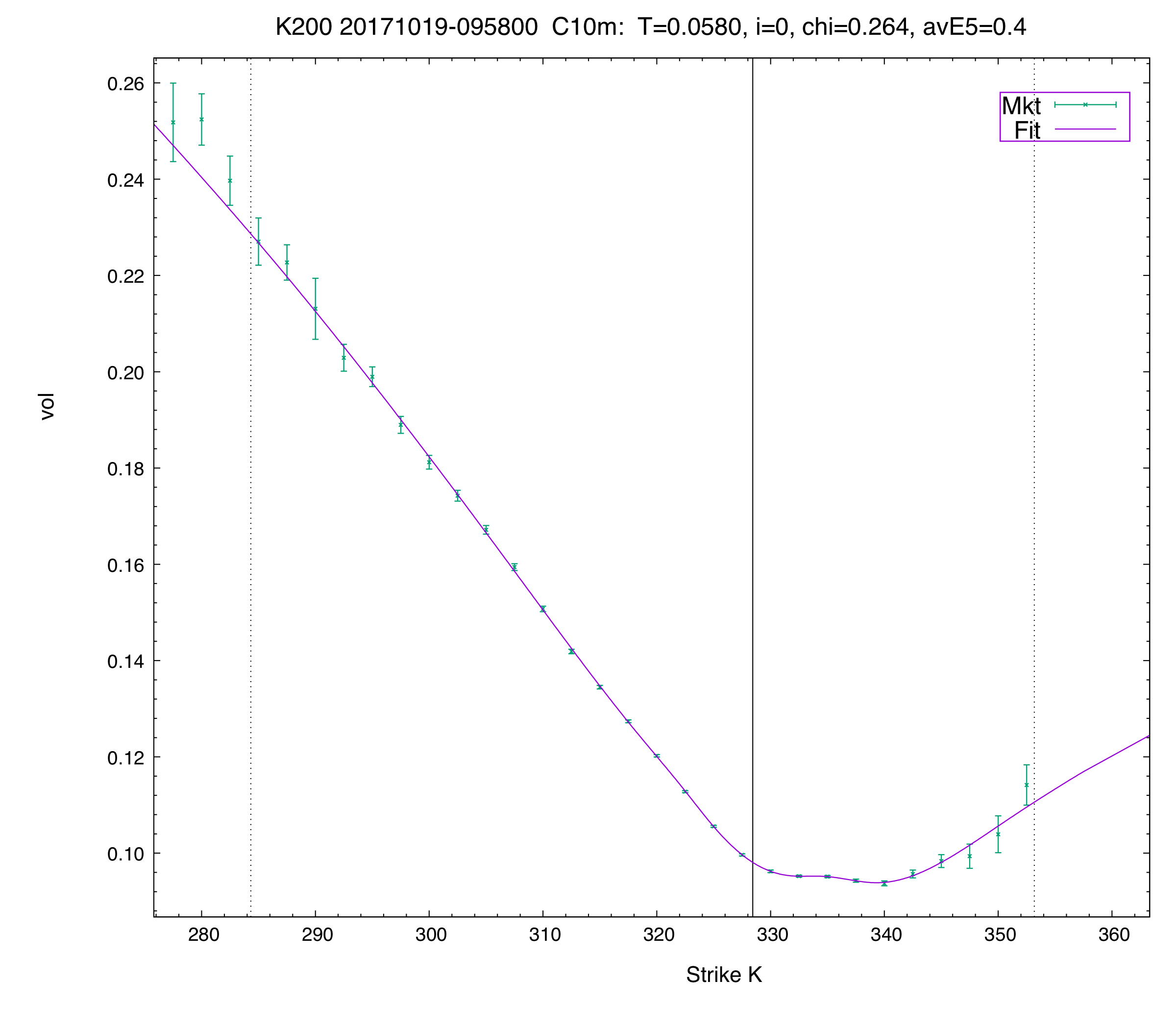

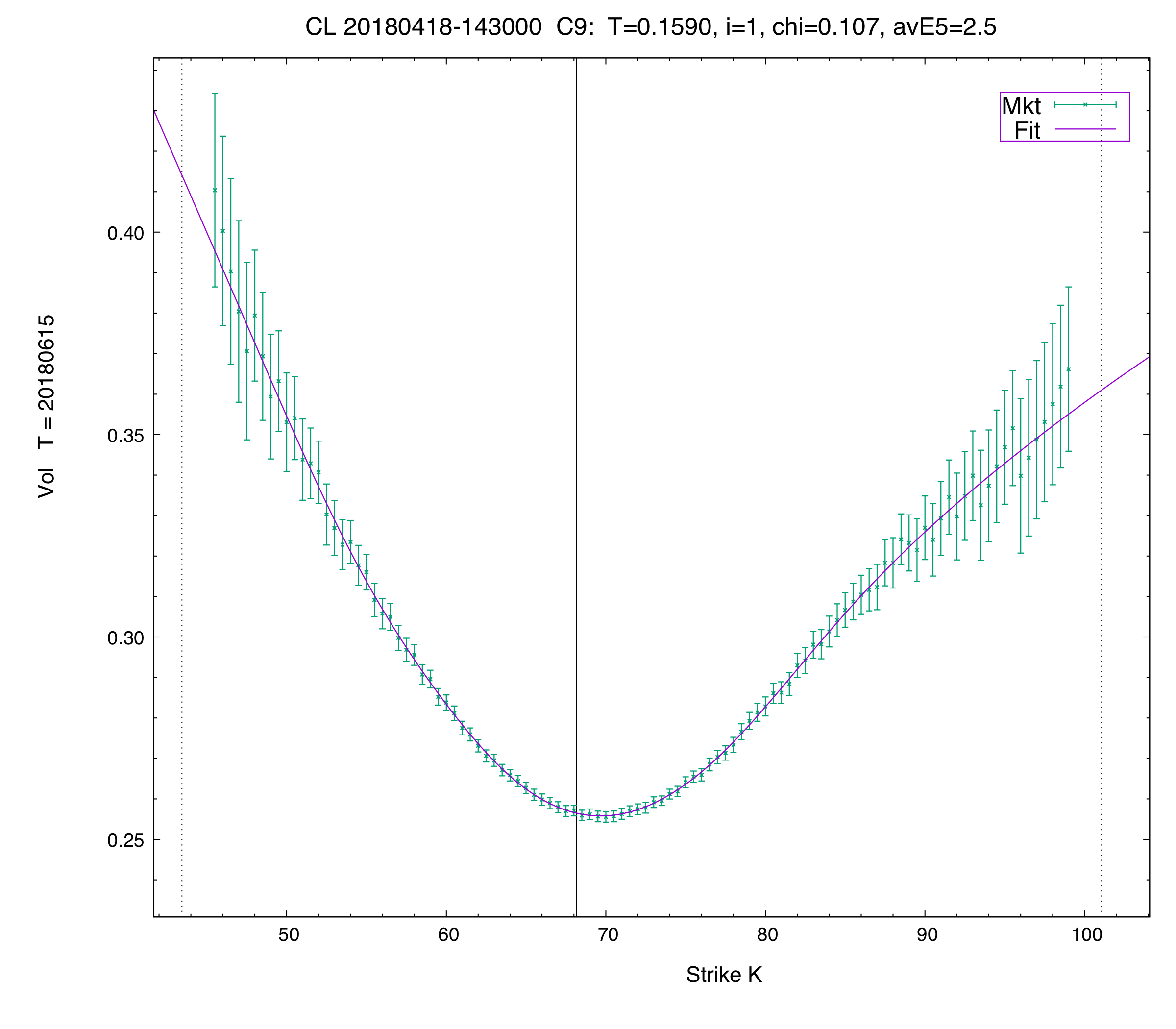

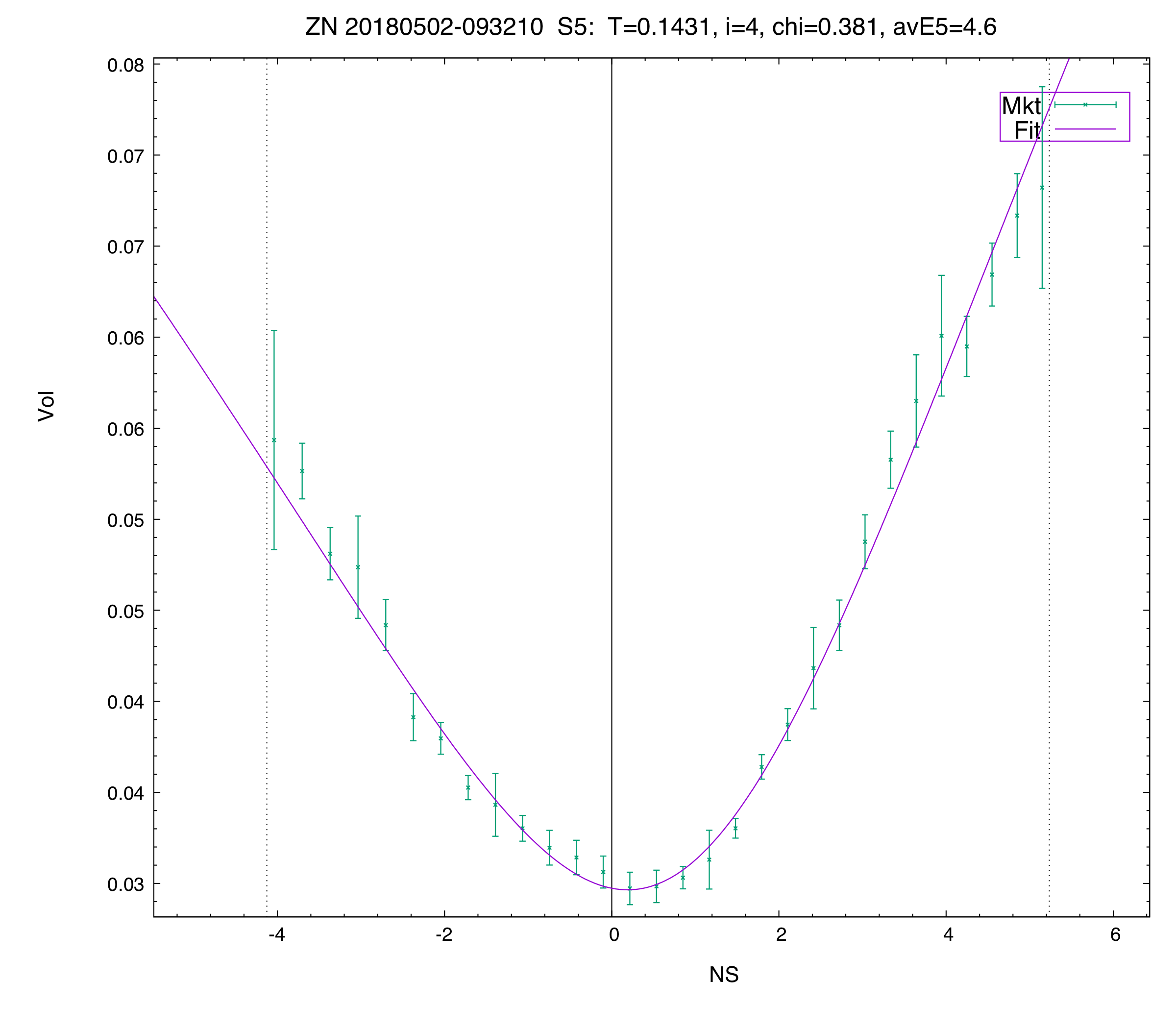

- Battle-tested through the COVID crash (VIX > 80), GameStop short squeeze (500%+ IV), negative oil prices, and 0DTE — no manual intervention, no parameter tuning required. See examples.

- Handles 0DTE and daily expirations — where even small input errors produce large vol errors and the surface shape changes rapidly intraday.

- Easily create and manipulate vol curves and surfaces to fit any market.

- We offer an intuitive and flexible family of nested parametric curves, way beyond standard curves like SSVI and SVI (which we also offer).

- Curves allow the fitting of options on liquid ETFs like SPY and futures like ES, CL, and even the W-shaped volatility curves of tech names like SPX, SPY, ES, NVDA, TSLA, etc, around earnings. No such curves are available anywhere else.

- Easily manipulate overall vol level and curve shape (ATF skew & curvature, and each wing independently).

- Easily switch between different curve types.

- Sensible book-level sensitivities to intuitive parameters, even across curve types.

- Curves can be used in a real-time fitter (see Fitter), or managed “by hand” if desired.

- The C* curves are a nested hierarchy of increasing flexibility. Different curve types can be specified per-expiry, and the Vol Curve Type Selector can recommend the right one automatically.

- Use greeks or scenarios to analyse your PnL for vanilla and vol derivatives.

- Explain PnL on an instrument or portfolio level.

- For PnL explanation with greeks, use smart or BS greeks. Smart greeks produce a cleaner decomposition because they account for the spot-vol relationship.

- For PnL explanation with scenarios, re-price the portfolio under specific factor shifts (spot, vol, time, rates, model changes). Exact — no approximation.

- Breakdown of vol PnL into ATF (level), skew (slope), curvature, and unexplained — showing what changed about the vol surface, not just that “vol moved.”

- Consistently attribute PnL for both vanilla and vol derivatives.

Use PnL Explanation to:

- Spot errors: Inconsistencies between your risk system and valuation framework immediately surface as unexplained PnL.

- Attribute edge: Determine whether a desk’s P&L comes from the factors they intended to trade or from accidental unhedged exposure.

- Optimize execution: Run PnL attribution on fills at different horizons and for different counterparties to reveal which factors need hedging and when.

- Validate models: If Greek-based and scenario-based attribution broadly agree, your framework is consistent. Material divergence is itself diagnostic.

See also Event Var Fitter and Event Modeling for separating event-driven PnL from background volatility PnL.

Trusted by Experts

Our clients trust Vola Dynamics to maintain their core valuation and risk analytics (pricing, greeks, volatility surface fitting, scenario analysis) for equity, futures and index options.