Example

Commodity Futures Options

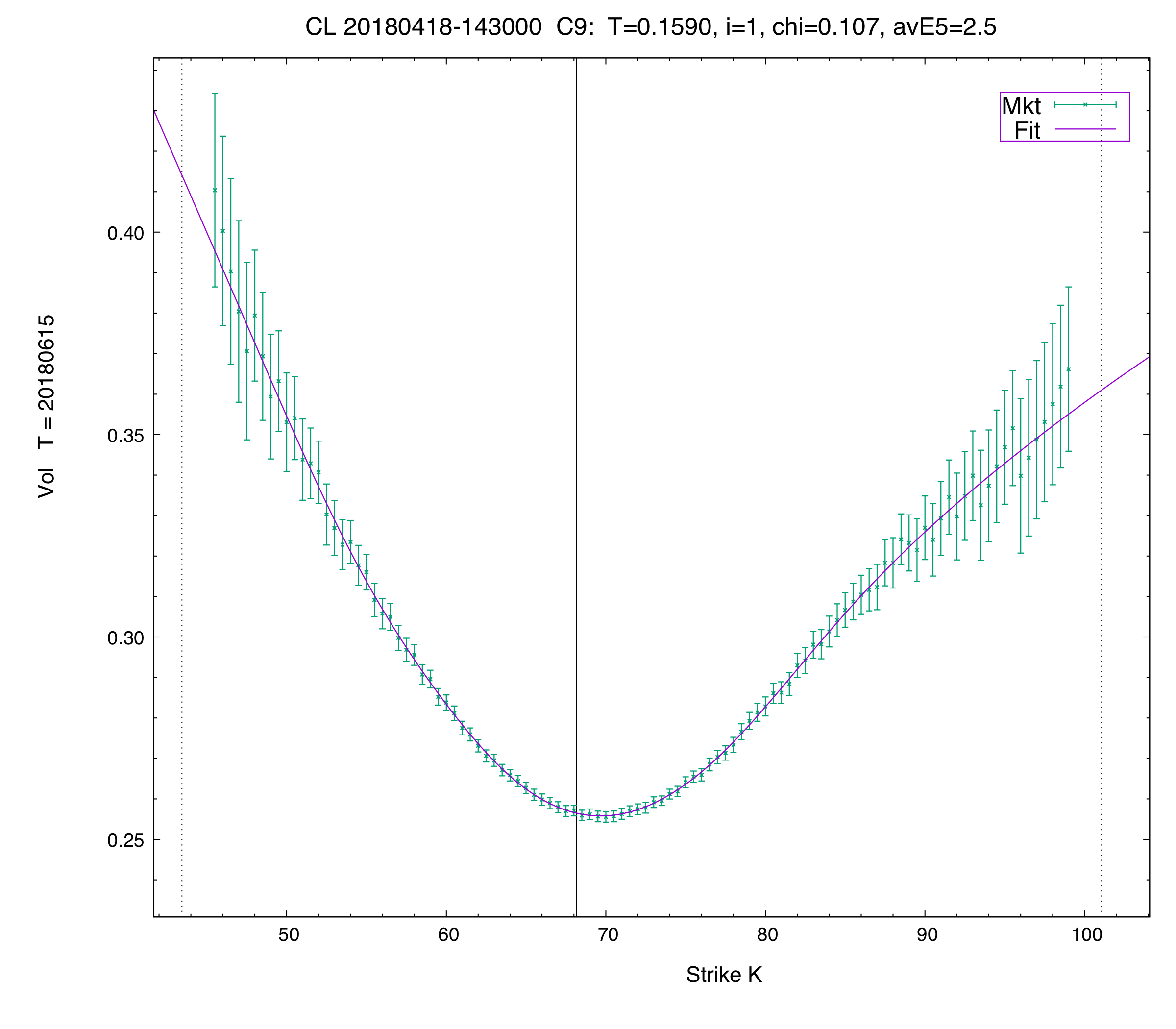

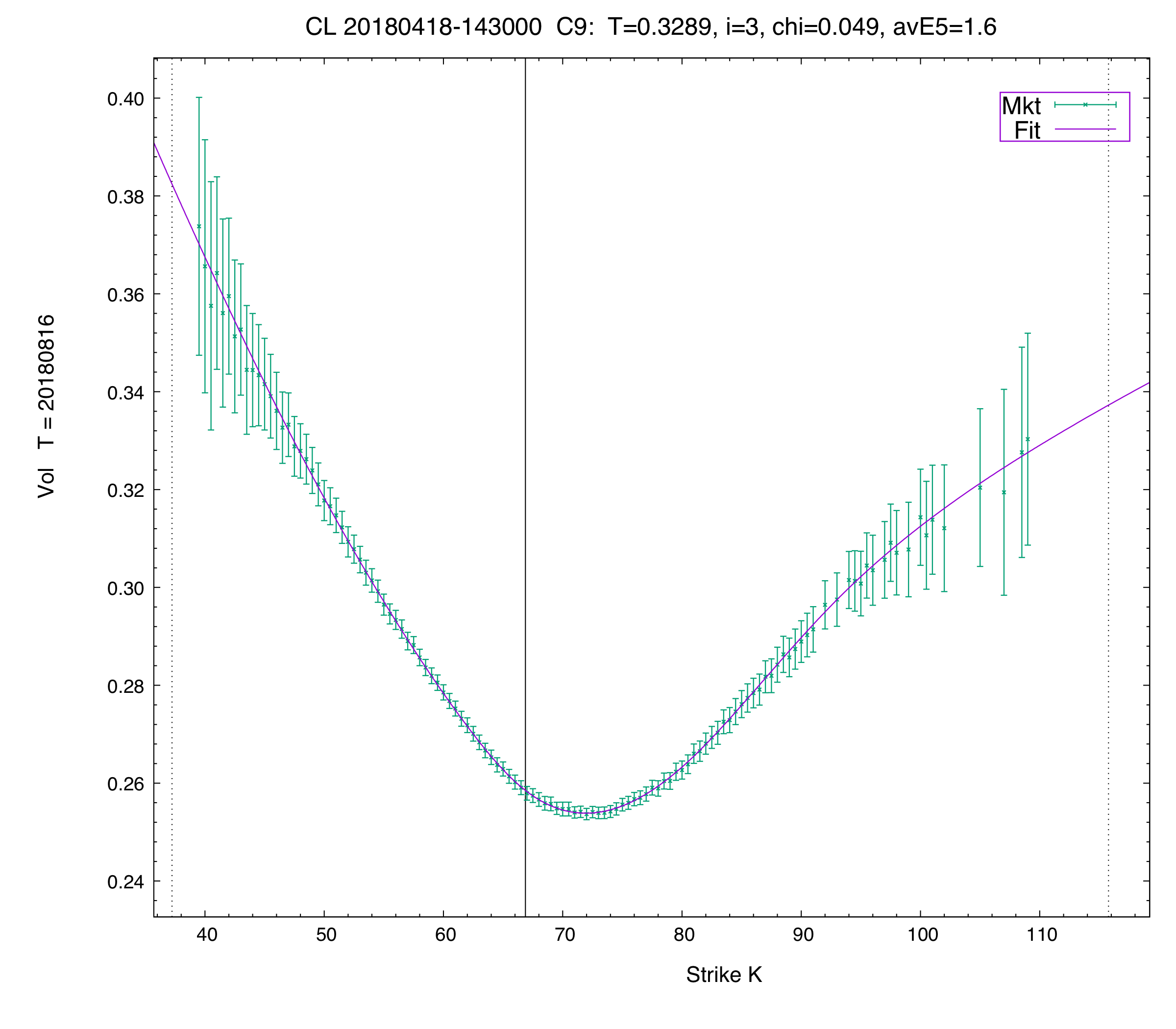

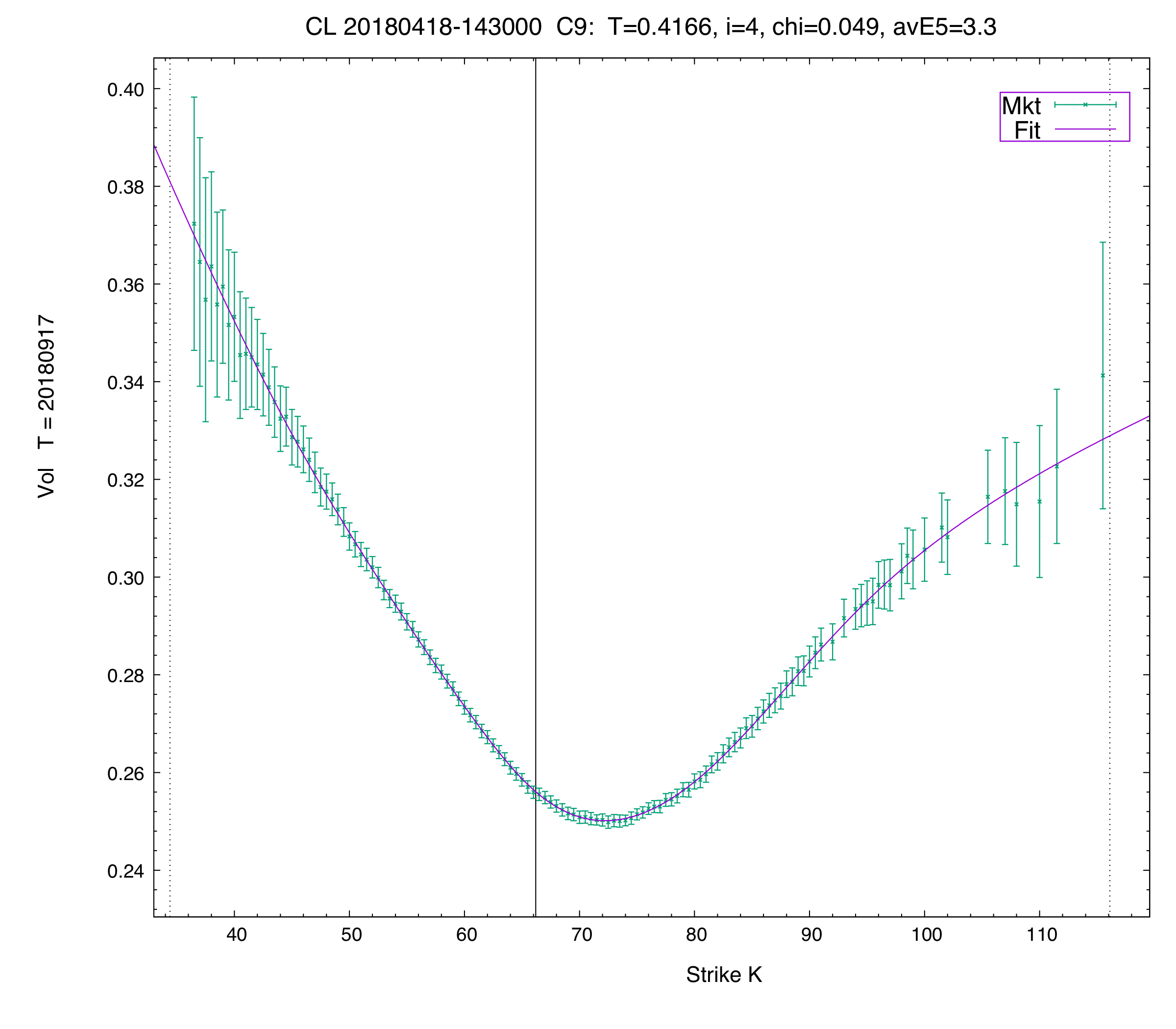

Just like for equity and index options, our robust fitter allows easy and fast calibration of tradable volcurves for futures options. In fact, one of our first clients has been trading crude options off our volcurves since early 2016.

Here we show fits for a couple of expiries on a snapshot of the market. Note that there are a lot of strikes and all expiries can be fitted well with the C9 curve.

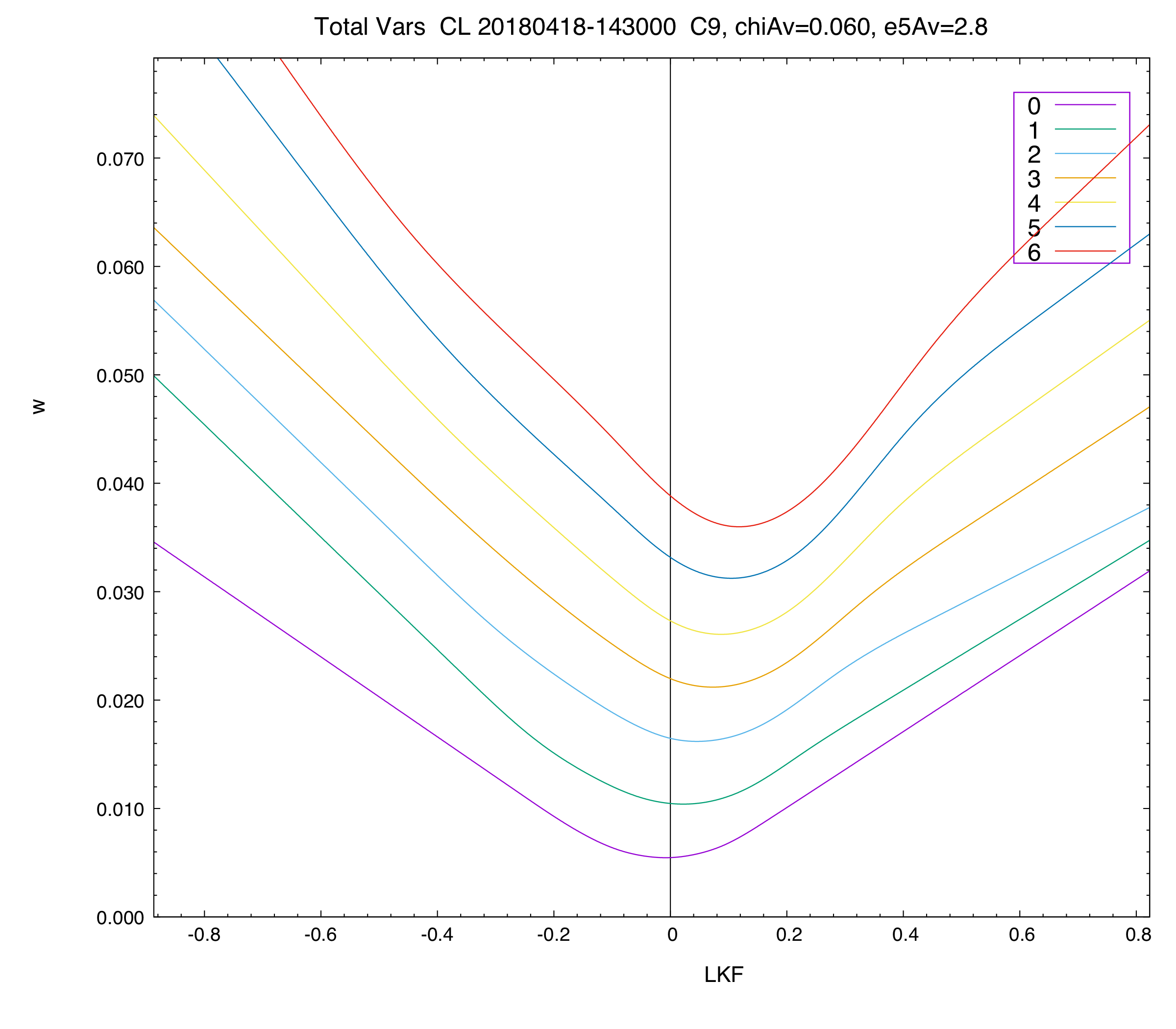

The volsurface is, off course, completely free of butterfly and calendar arbitrage. The latter is illustrated by the total variance plot.